Retail banks can expand and thrive in unprecedented ways thanks to the advancement and diversity of technology and more access to data. User-related database holds great potential for retail banks to generate new revenue streams.

To be able to unlock such new potential, retail banks first need to answer a fundamental question: How is the bank envisioning its future? This article will offer four main trends for retail banks to better orient themselves in the future. However, to fully answer the aforementioned question, it is vital that banks know their direction and what tools are needed to pursue the chosen path.

4 Trends Shaping the Future of Retail Banking (1)

Customer-centric digital banking: The focus of retail banking is to directly provide products and services that the bank itself knows are suitable for customer needs and distribute them in a way that attracts users thanks to the bank’s unique insights into customer tastes and habits.

Importantly, these products do not need to be owned by a bank but are taken from the market and offered to customers who will benefit from these products.

Banking as a platform provider: The focus of retail banking is to connect different providers, in order to provide the foundation for the broader ecosystem to be capable of collating the data flows, based on the open and easily accessible infrastructure provided by that bank.

Retail banking positions into product specialization: Retail banking creates products that have a competitive advantage thanks to their deep knowledge and experience of the market as well as the ability to quickly create new products to meet market demands. The bank is pursuing a part of the value chain. These products are ready so that other suppliers in the market can use detailed information about their customers to find the right customers for the product.

Banking as a utility provider: Banks that have established strong infrastructure are able to provide for many partners in the niche market (also known as niche players) who are present across the rest of the ecosystem. Banks aiming for such positioning can provide white-labeled services (the brand name is not displayed on the final product) for core banking infrastructure such as payments, processing, clearing, etc.

These four main trends will shift the business model of retail banking from the traditional business model (monolithic – organized as a large block, slow to change, only providing in-house products) to an ecosystem of retail banking. By then, the banking ecosystem will have inter-interactions and the ability to ensure that customer service services are seamless between different products and services.

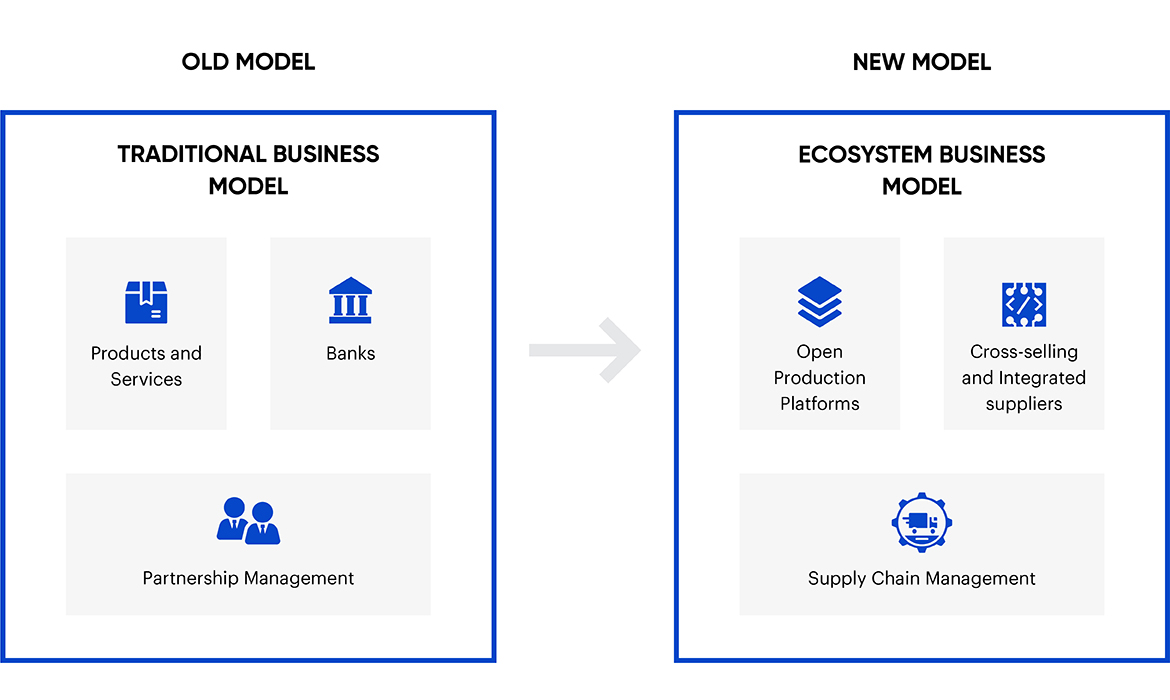

The market remains competitive, but the competition is defined by the ability to drive value on one or several components of an overall system that requires the involvement of multiple suppliers, rather than just viewing each bank act as a similar monolithic institution, competing directly with each other. The following figure will illustrate the shift from a traditional business model to an ecosystem business model:

Banks following the traditional business model have 3 main components:

- Products and services: These are directly provided to customers by retail banks

- Bank: Positions itself as a brand that only offers the products it creates

- Partnership Management: The retail bank manages partners in its supply chain

Shifting to the ecosystem business model will lead to tremendous changes in these 3 components:

- From making products and services to harnessing the power of open product platforms

- From playing the role of only providing in-house products to being able to integrate, cross-sell with other suppliers such as other banks, fintech companies, etc.

- From managing a number of closely connected partners to managing supply chains to find new customers offered by the ecosystem

Strategies to gain value from data

Corresponding to the four main trends shaping the future of retail banking must be the data strategies to maximize the value of data to achieve the future vision.

Data strategy helps banks become more customer-centric: The bank’s data investment will revolve around creating and protecting digital brands, personalizing the customer experience, managing the value brought to customers, and data security (since bank data is the main competitive advantage). Globally known banks that choose a positioning strategy focusing on synchronization associated with data strategy are Monzo Bank Ltd from the United Kingdom, TD Bank from Canada,…

Data strategy helps banks become a platform provider: The bank’s data investment will be based on APIs communication gateways (which allow connections with other applications and software) and will collect data from which the bank can profit to attract other organizations to the platform. With this positioning, personalization is not as important as easy access, although this is definitely a place where the boundaries between product categories are blurred.

Selling insights related to the foundation is the most important opportunity. Using this strategy, Moven and Yodlee are both aiming to provide a platform-based approach to bring together products from different banks. However, an open banking policy or similar policy will help shape this orientation.

Data strategy helps retail banking position into product specialization: The bank’s data investment will be based on APIs (capable of integrating into the processes of other organizations such as other banks, fintech companies, etc.) and market research to recognize the value and management efficiency of the product. This market space is ideally suitable for today’s well-known banking companies.

Data strategy helps banks become utility providers: The bank’s data investment will be based on process efficiency, automation, and cost reduction and vary depending on service levels. Personalizing and marketing the product is irrelevant in this case, instead, seamless back-end infrastructure and speed are key. Clear Bank from the UK, Fidor Bank from Germany, and BNY Mellon from the US are now positioned in this market space and offer similar services.

Comprehensive and consistent data strategy framework

A huge challenge for retail banks after the leaders outline the positioning vision and data strategy in sync with the vision is how to turn the vision and strategy into reality while taking advantage of the competitive advantage, using the optimal resource while following the law, international standards and maximizing the power brought about by the ecosystem network.

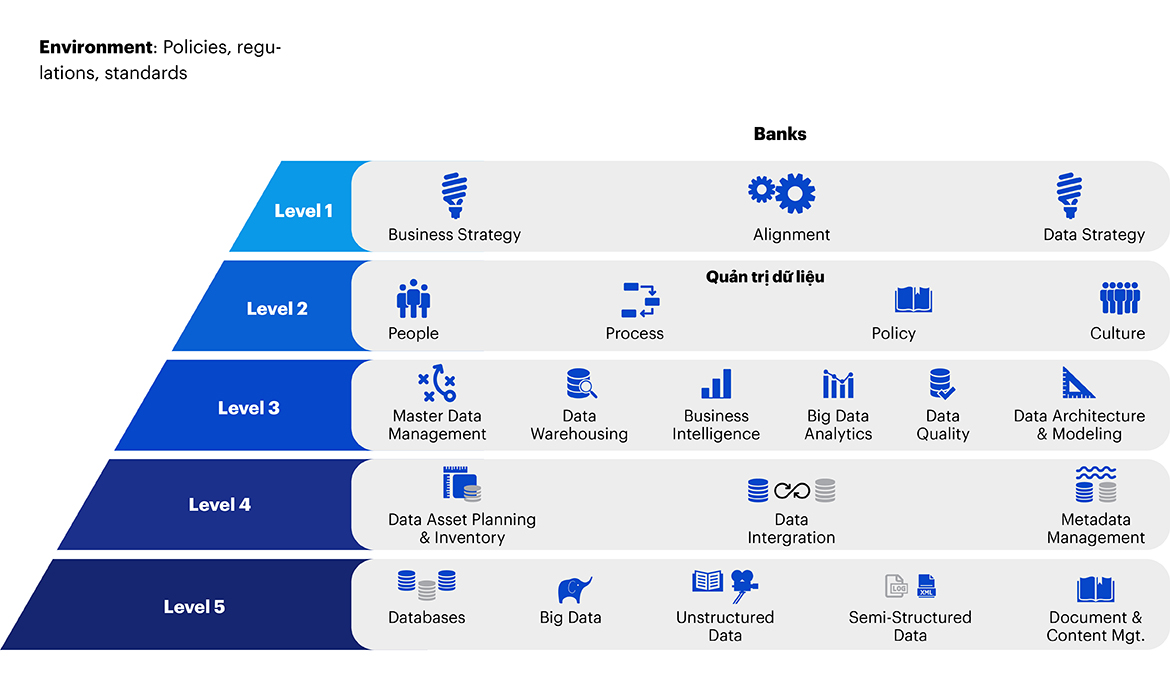

The data strategy framework is divided into two main spaces: Environment and Banks. Environment is a non-banking business environment bound by international or national policies, regulations or standards. Banks can call on authorities to come up with appropriate policies such as data privacy policies for customers, open banks, platform licensing, APIs standards, etc., on which to base for practical application(3).

Banks is an internal expression in a bank with 5 levels. The bank has the initiative to create overall consistent strength and exploit the entire ecosystem. The data strategy framework approach shown in the following figure will make it easier for banks to overcome these challenges:

Level 1: Developing a data strategy requires synchronous alignment with business strategy. An example is a data strategy to help a bank become a customer-centric digital bank.

Level 2: Data governance plays an important role in managing people, processes, internal policies and culture around data. This is a non-technological issue that requires change, upgrading for each worker who needs new skills, to changes in the process chain (e.g., shortening the process due to automation), to new policies or changes in working habits and culture due to data being mounted in day-to-day operations.

Level 3: Leverage and manage data for strategic advantages. For example, big data analytics helps manage risk by relying on real-time analysis of user behaviors to minimize potential risks.

Level 4: Coordinate and integrate different data sources to maximize value. With the ecosystem network formed, banks can integrate fintech company data sources to bring a better experience to customers with the right products.

Level 5: Data management and inventory to maximize value while in accordance with international laws and standards.

Retail banking aspiring to shape the future and turn the vision into reality based on data strategy can follow these steps, from positioning a vision associated with a competitive advantage, building a value-creating data strategy that is aligned with the vision, and creatively applying a data strategy framework so as to develop the bank in accordance with international laws and standards and utilize internal strength and network strength of the ecosystem.

Reference sources:

(1) Accenture. What Bank do you want to be

(2) Globaldata Strategy

(3) Bank magazine