The term Open Banking first appeared in the Revised Payment Services Directive (PSD2) of the European Union (EU, 2015). Accordingly to PSD2, Open Banking allows third-party payment service providers to access customers’ banking data information through the secure Open Application Programming Interface (Open API).

The initial objectives of open banking were to create a more complete payments market, making payments more secure and protecting consumers better. However, open banking has become a revolutionary trend and is one of the requirements in the roadmap towards digital banking in the present and the future.

New “players”

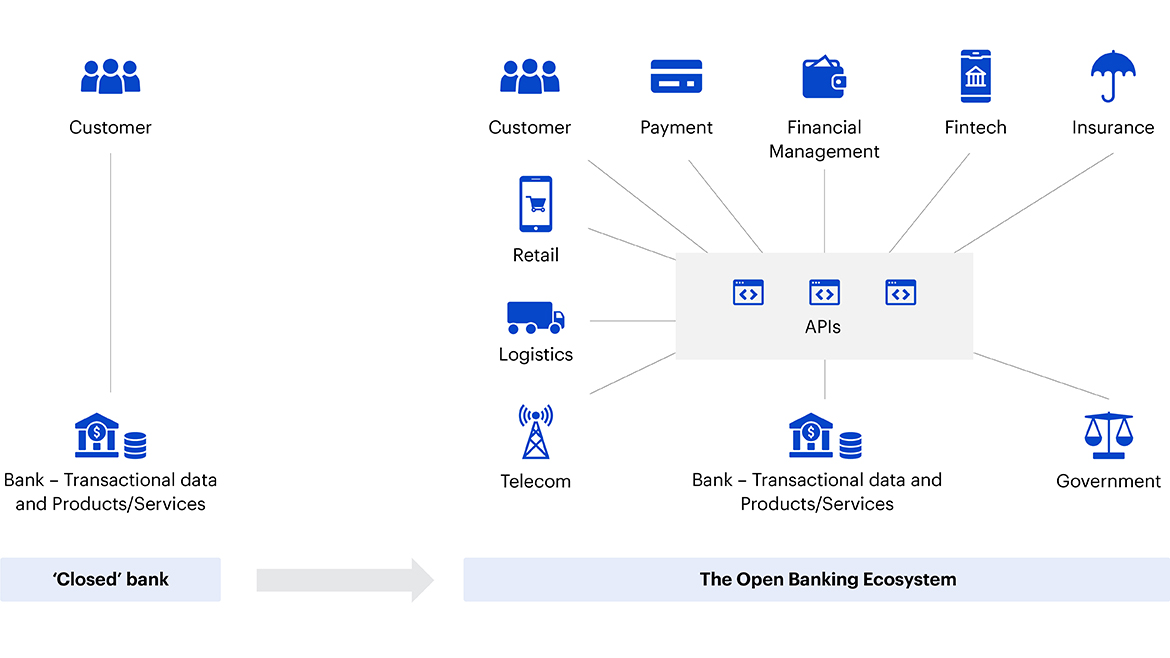

In the past, most banks offered and controlled products and services on their own proprietary distribution channels such as transaction offices and online banking. The experience of the bank’s operations is completely “closed” to the external business environment, the sharing of data information even with the customers themselves is very limited.

The rise of fintech in recent years has created new playgrounds, new business models with new players, disrupting the “closed” position of traditional financial institutions. Following the inevitable flow of the sharing economy, traditional banks have been aware that new players, including fintech businesses, big technology companies, payment service providers, and financial management, are not hazards or direct competitors but partners to exploit the potential of the ever-expanding market.

Open banking ecosystem

Traditional banks have the strength of business platforms, large customer bases, and transaction data warehouses, which can be shared with authorized third-party service providers to access and exploit information, together with the needs and interests of consumers:

- The right to access financial data and its transparency.

- Personalized experience of products and services.

- There are many options for better decision making, supporting in improving the competitive efficiency of products and services.

At the same time, banks and financial institutions also receive significant benefits from open banking such as optimizing processes, reducing costs and transaction times, expanding access to customers who do not have bank accounts, increasing utility products and services, and revenue, increasing customer loyalty, and satisfaction through data analysis activities.

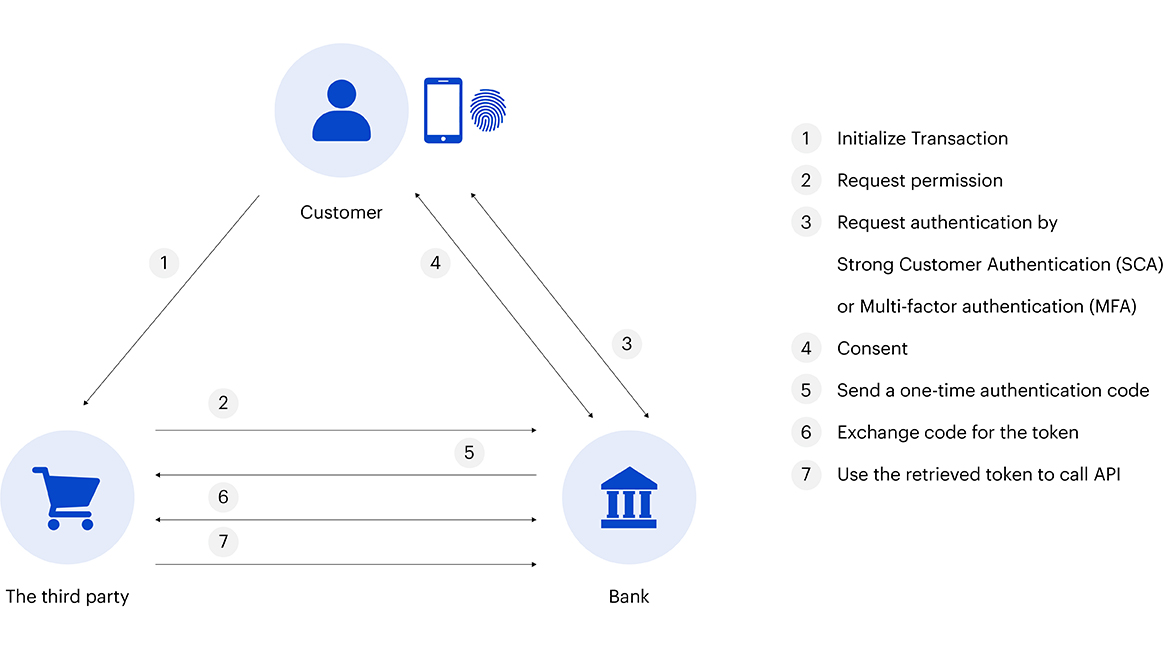

Is open banking safe and secure?

From the perspective of managers and strategic planners, despite many benefits, open banking still raises concerns about privacy and data security. However, in terms of technical infrastructure, the development and improvement of Open API play a backbone role in the implementation of open banking and have been eliminating concerns towards the goal.

The following is a security protocol diagram when a third-party service provider asks the bank-side API to execute the transaction.

In parallel with standardizing security protocols, technology companies simultaneously provide fast-growing lifecycle management solutions and platforms in the number of open APIs, ensuring synchronous optimization, stability, and operational control.

The current situation and direction of open banking

Global context

2018 is considered the beginning of the open banking era. Practically on a global scale, many countries of the European Union, UK, Japan, Singapore, Hong Kong, Australia, etc., already have specific strategies and policies in place to develop a regulatory framework that underpins the development of open banking. At the same time, open banking projects that have been implemented in recent years have been positively received.

Consultants and researchers have also proposed models to assess the maturity of open banks for countries and banking institutions based on criteria related to the readiness of the legal framework, the scale of partner growth in the ecosystem, the data platform as well as the quantity and quality of the open API category. The results of the assessment will help determine the current situation, orientation for the development of roadmaps, and appropriate action programs for the development of open banking.

Vietnam

In Vietnam, although there is no legal framework for open banking, many banks are applying open API technology to open connections with payment intermediaries, e-commerce, and utility service providers such as electricity, water, and transportation. Several big names have taken pioneering steps, including VietinBank, OCB, Agribank, TPBank, BIDV, VPBank, Vietcombank, etc.

The drawback is that the open APIs currently applied by banks are only bilateral connections between banks and partner units which do not have a unified common standard. Besides, there are potential risks related to customer data information, the quality and stability of open APIs, the accuracy and reliability of the data exchanged.

The State Bank of Vietnam (SBV) has also initially developed, tested, and gradually perfected legal frameworks to manage open banking activities in the spirit of the Prime Minister’s Directive No. 16/CT-TTg on strengthening the capacity to approach industry 4.0. The Governor of the SBV has established the Steering Committee on fintech under Decision No. 328/QD-NHNN dated March 16, 2017. Therefore, the research and development of data connection and sharing through the open API are some of the key tasks of the Committee.

Recommendations for legal frameworks should include the Law on the protection of privacy and user data, the Decree for electronic identification and authentication activities, as well as standards and guidelines on technical and information technology infrastructure.

On the bank side, it is necessary to take the initiative proactively in developing a transformation strategy, preparing data organization and appropriate technology solutions.