AI (Artificial Intelligence) is a technology that simulates human thought and learning processes for machines. AI used to be something that only existed in the human imagination and fiction movies decades ago, but now it has gradually become popular in our daily lives. More specifically, what is AI?

1. Overview of AI

AI refers to the ability of computers or machines to mimic the capacities of the human mind and learn from previous experiences to understand and respond to languages, make decisions, and solve problems. AI uses large amounts of data information to train and develop algorithms that allow machines to acquire capabilities that closely resemble humans.

The ecosystem of AI technology currently includes machine learning, robotics, artificial neural networks, and natural language processing – NLP. There are different applications of AI, such as Facial Recognition, Speech processing, Crowd counting & estimation, Cyber security, and security.

The characteristic of AI technology is the “self-learning” ability of computers so the computer can judge and analyze data in advance without human support, and be able to process data in large quantities at high speed.

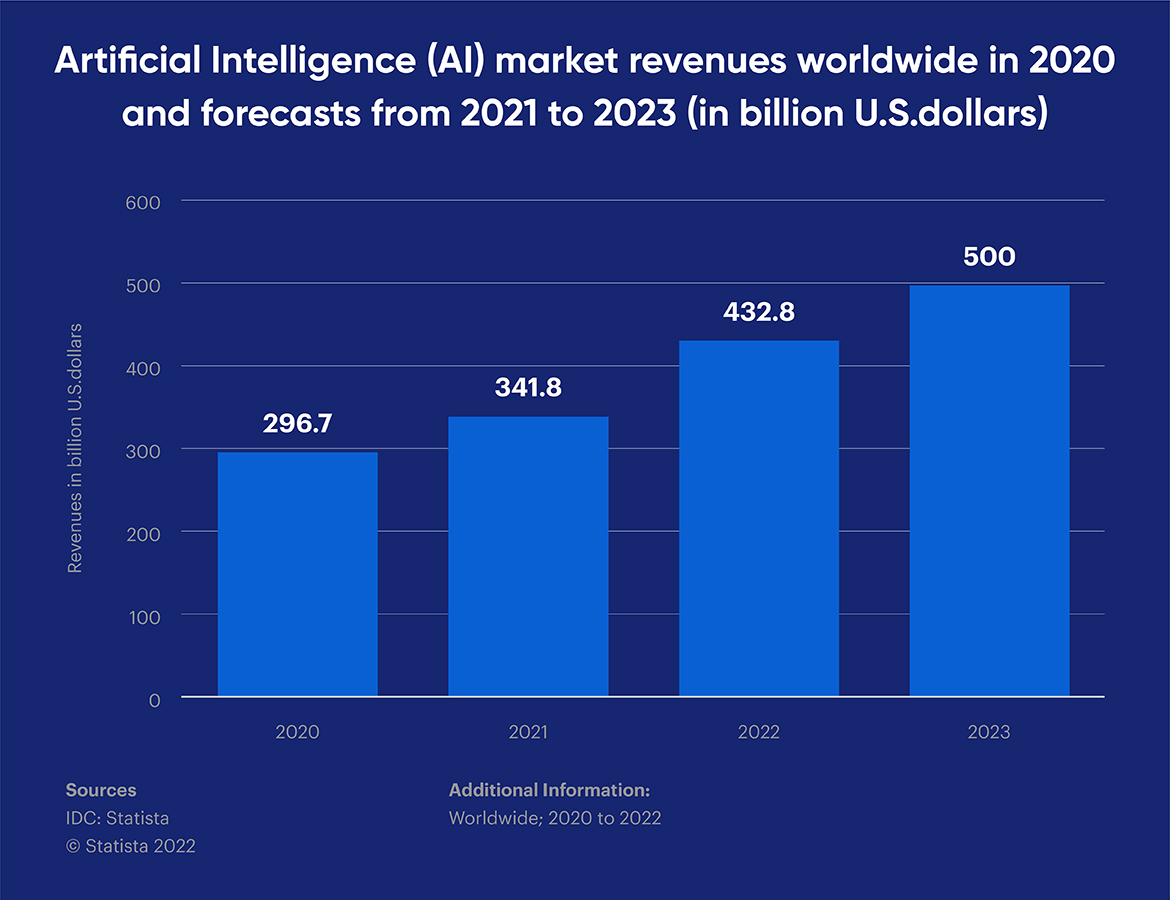

According to research from IDC, global AI market revenue in 2021 is estimated at $341.8 billion and is forecast to reach $500 billion by 2023(1).

2. AI technology in the insurance industry

In the development process associated with AI technology, Insurance companies need to make a gradual transition from a state of “detection and repair” to “anticipate and prevent” problems that may occur to their insurance subjects. The pace of transformation also needs to increase rapidly as consumers, intermediaries of insurance companies, or suppliers become more adept at using technology to improve productivity, make decisions, reduce costs, and optimize the customer experience.

As AI integrates deeper into the insurance industry, leaders of insurance companies and providers need to understand the factors that make the change and how AI will reshape requirements, distribution, underwriting, and pricing requirements. Also, repositioning in a constantly changing business landscape is critical to becoming successful players in the current and future insurance industry.

In a Deloitte 2021 survey with insurers, 12% of respondents expected a sharp increase in AI spending, and 28% of companies expected a slight increase in spending on AI technology in the insurance industry.2 According to a Genpact survey, 87% of Insurance companies invest more than $5 million annually in AI technology. Among Insurance companies that have invested in AI, many have reaped remarkable benefits. Nearly 50% of companies believe that AI is helping to improve decision-making. According to a PwC report working with insurers on AI initiatives, these companies are increasingly using AI to contribute to:

- Customize products for both consumers and business customers.

- Create more continuous customer interactions to earn their loyalty and higher sales capabilities.

- Analyze more data from more sources (including social media channels) for better forecasting.

- Automate many aspects of the complaints processing process.

- Enhance the detection and classification of fraud problems.

- Conduct asset analyses and more sophisticated insurance calculations.

3. What AI technology has been contributing to the insurance industry

The past two years have been difficult for most insurance companies, but it also reinforces the importance of technology, especially AI, to the field.

3.1 AI assists in claims processing in insurance claims

The majority of the work involved in claim management is paper-based and manual. This makes work error-prone and inefficient, leading to increased operating costs for insurance companies.

To solve that problem, many insurance companies have planned to operate businesses with the support of technologies such as AI, RPA, and IoT … With IoT support, insurers can automatically collect more comprehensive customer data. With the large amount of data collected, AI algorithms can prioritize scanning all incoming data and check customer verification most accurately and efficiently to help solve problems faster.

Some cases where AI helps with claims processing:

3.2 Speed up processing of insurance refund claims

Using machine learning to understand and process customer requests allows insurers to increase efficiency in data administration processes. By extracting insights from various data sources and putting them into processing, analytics can help improve the quality of risk assessment, resulting in better valuations for insurance claims.

Insurance providers and customers alike want every process to happen quickly. AI enables speed up by taking on some of the product inspection work that requires insurance. The AI system combines with other supporting equipment to ensure safe and fast appraisal and evidence collection sessions.

A real-life example is Tokio Marine implementing image identification to estimate the cost of vehicle repairs. The automotive company has deployed an AI-based computer vision system to inspect and evaluate damaged vehicles. Thereby, Tokio Marine can speed up the review requests and significantly shorten the processing time instead of taking 2-3 weeks (the average processing time in Japan).

3.3 Digitize data quickly when using computer vision – OCR

OCR stands for optical character recognition – a process that uses technology to recognize digits and handwritten text, which insurers can use as a tool to change their game. Instead of having employees manually re-enter data but also prone to errors, insurance companies can empower systems to automatically collect and collate data from different forms. OCR can accurately display each piece of information on the form and convert it to the corresponding digital form. Increasing automation in data digitization helps insurers save up to 80% on costs for each process (4).

3.4 Conduct guarantees more quickly and accurately

Rules-based assessments and risk-inducing motives in the guarantee process are no longer sufficient to provide accurate information for insurance providers, especially as the types of scenarios are more diverse and the level of fraud has become more sophisticated. Computer vision technology combined with IoT data can assist insurers in recording the status of assets at the time of the guarantee and subsequent execution states during real-time processing, which helps prevent any possible negative behavior.

3.5 Detecting and preventing fraud in insurance claims

Technology not only increases the amount of information so that underwriters and risk managers can easily make decisions but also increase both quality and support for processing them. Insurance fraud occurs a lot causing insurance companies to lose a large amount of money to pay for this problem. The cause of such a situation is understandable as most still rely on outdated systems and sets of rules without the ability to detect complex fraud schemes.

AI-powered fraud detection systems address most of the shortcomings of previous applications while enhancing analysts’ judgment by providing them with more valuable information. Machine learning and deep learning systems are capable of identifying repeating patterns that support agile algorithms that capture unusual behaviors in the system or between individual customers. Thanks to this support from

technology, insurance companies will detect, prevent and significantly reduce fraud on the part of customers and the risks to their company.

3.6 Increase customer base with competitive premiums for drivers

Using AI to analyze data helps insurance companies to reach potential customers. The detailed information from the analysis allows insurance companies to promote and continuously improve operational efficiency. When there is more information about customers, insurance providers easily convince them to buy equivalent products (sell more) or products related to the product they already have (sold).

Also, insurance providers can advise drivers to use another product in exchange for a premium discount. AI algorithms help collect and analyze customer data information such as the credit history of the policyholder, spending habits, and occupations … to customize and provide insurance prices, personalized services, and experiences; this increases the opportunity to sell and expands the customer base.

3.7 Actions of Vietnamese insurers to keep up with industry trends

Over the years, Vietnam’s insurance industry has started implementing AI into the insurance business. However, insurance companies still apply AI much more slowly than other industries.

Some Vietnamese insurance companies have applied AI technology to provide better pricing policies for customers. They also integrate AI deployment at customer contact stages, customer service management, and support (such as chatbots, and virtual assistants) to provide a seamless digital experience and improve customer satisfaction.

Deploying AI into operational processes allows insurance companies to save time, and costs, improve customer experience, and increase profitability. AI also helps reduce human errors that come from the input process or changes in information regulation for analysis to prevent fraud.

3.8 The Future of AI Technology

After the Covid-19 outbreak, the insurance industry has emerged as a great opportunity but will also be under high pressure. With the trend of technology development and application in social life constantly changing, AI technology has become a destination for more scientists in the future, which contributes to supporting most industries, especially the insurance industry. With the trend of bringing a better experience to customers focused on developing in the current Vietnamese market, the future of AI development in this market is very open and not too far away.

Reference sources:

(1) Statista. 2022. Artificial intelligence (AI) market revenues worldwide in 2020 and forecasts from 2021 to 2023

(2) Statista. 2022. Digital technology investment priorities of insurance companies worldwide in 2020

(3) Genpact. n.d. The dawn of the age of AI in insurance

(4) McKinsey & Company. 2018. Evolving insurance cost structure